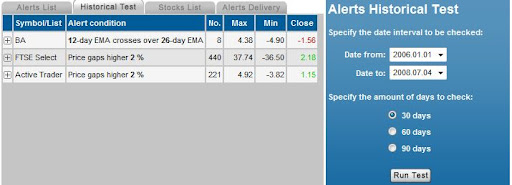

Note when creating an Advanced Alert it is necessary to create the individual component alerts before they can be combined as an Advanced Alert. Also, alerts for stocks can't be combined with those for stocklists.

Back to the test. I used the traditional bag of stocks:

Active Trader (US): AAPL, BA, C, CAT, CSCO, DIS, GM, HPQ, IBM, INTC, IP, JPM, KO, MSFT, SBUX, T, WMT

FTSE Select (UK): AGA_L, AVE_L, BB_L, BUR_L, COLT_L, CSR_L, DDT_L, DEB_L, DRX_L, FCAM_L, GFS_L, GNS_L, HIK_L, ISAT_L, LAD_L, LSE_L, MCRO_L, MGNS_L, NFDS_L, PFC_L, PFG_L, PNN_L, RGU_L, RRS_L, SCHE_L, TATE_L, TLW_L, UKC_L

Test Period: Jan 1st 2006 to Aug 1st 2008.

What is immediately apparent is the combination alert of the 2% gap and 120-day high together performed worse for US stocks than the component alerts did independently. There was no performance advantage using these two alerts in combination for UK stocks, but there was no disadvantage either.

In terms of the price range over the 1-, 2-, and 3-month periods; the Advanced Alert for U.S. stocks returned an average maximum gain of 5.8% to 17.4% from the trigger date, with maximum losses ranging from -15.3% to -21.3%. There was a more even spread across U.K. stocks with a maximum gain in the 6.2% to 12.1% range and a maximum loss of -6.7% to -10.7%.

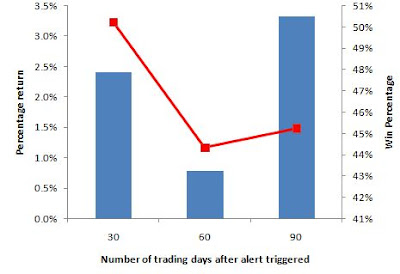

FTSE Select 1-, 2-, and 3-month returns:

Closing returns for U.K. stocks rose over time, although gains were minimal - even after 3 months.

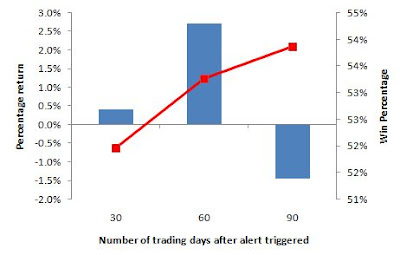

Active Trader Select 1-, 2-, and 3-month returns:

A horrendous short term performance over 1 month for U.S. stocks gave way to flat returns over subsequent 2 and 3 months.

Overall, this particularly combination of alerts was not one to set the world alight. There may even be reason to see this as a shorting play - although further testing involving proper risk management would be needed to confirm.

Dr. Declan Fallon, Senior Market Technician, Zignals.com the free stock alerts, market alerts, and stock charts website